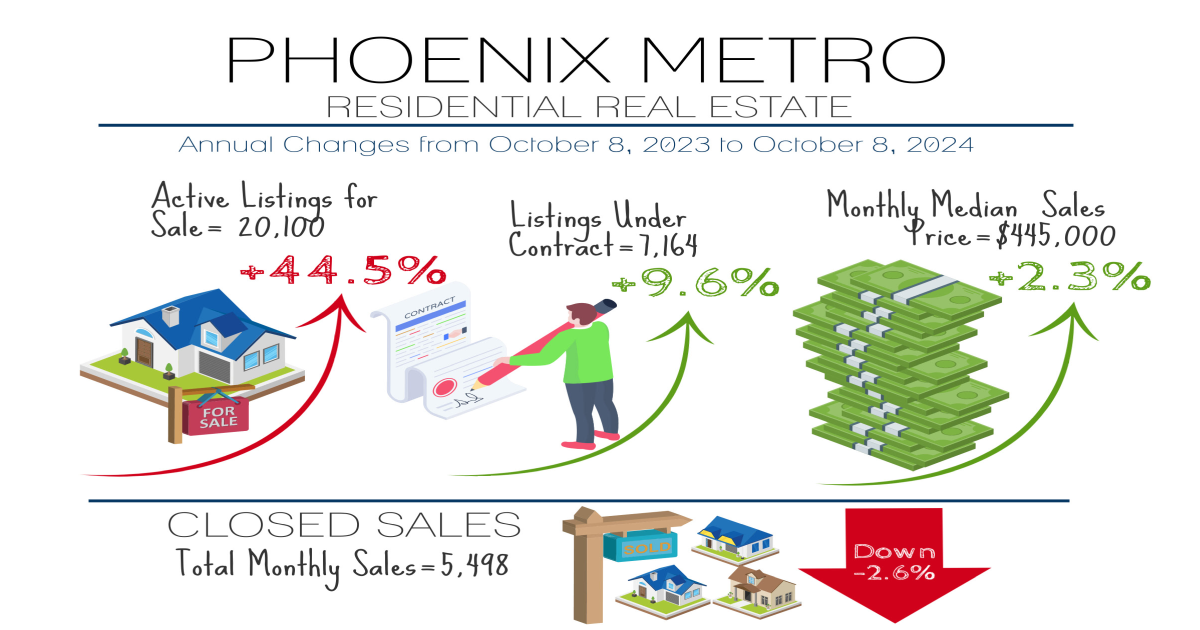

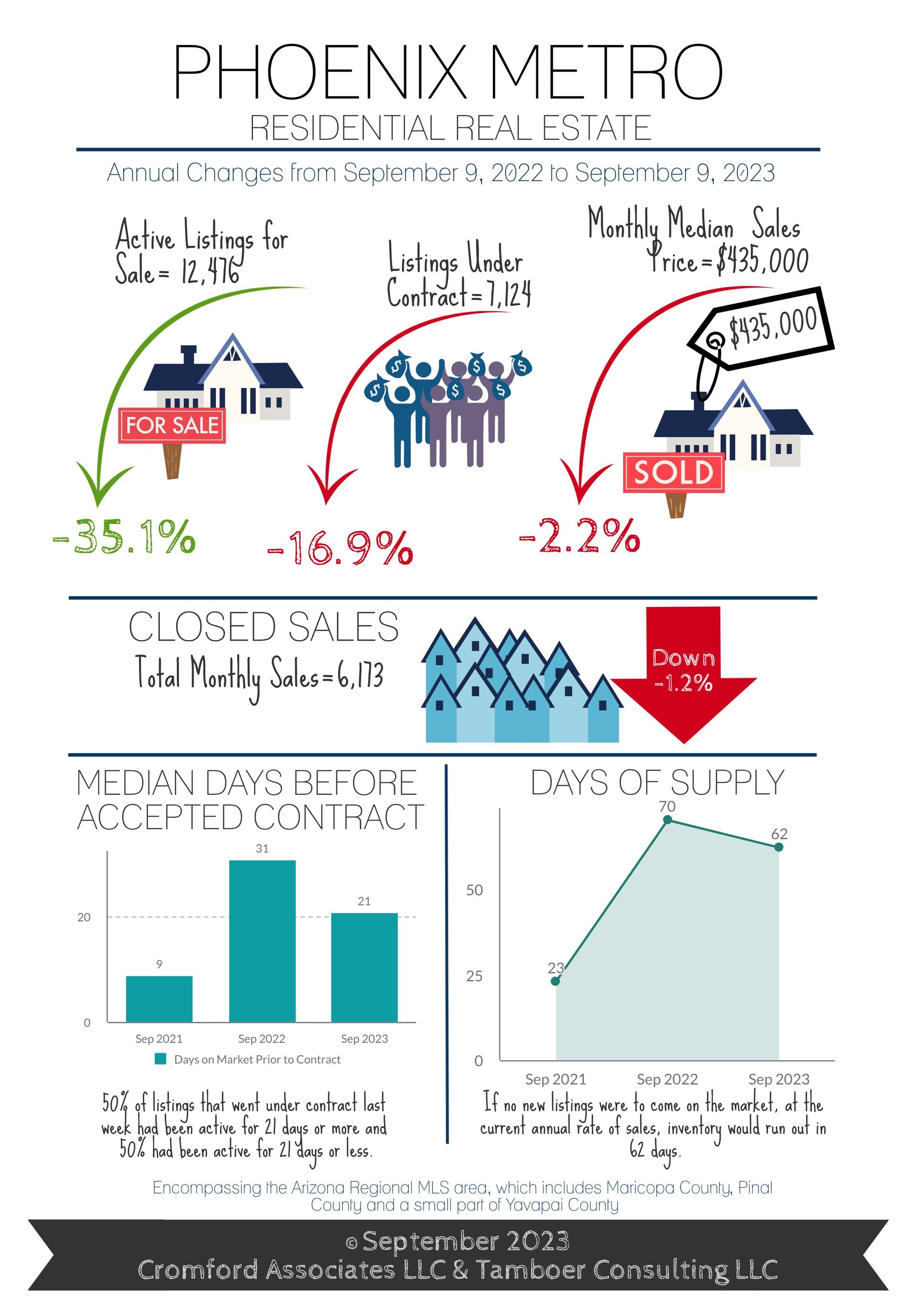

September 2023 Phoenix Real Estate Snapshot

Why Buyers Should Stay in the Game in 2023

Sellers: Prepare for Longer Days on Market in Q4

For Buyers:

When first-time home buyers talk to their parents or grandparents about today’s mortgage rates, they may get a response similar to, “I purchased my first home in the 80’s at [insert range of 10%-18% interest here].” In fact, some carry their high mortgage rate like a badge of honor because it turned out to be a great decision, despite the uncertainties of their time. In their 20s and early 30s, Baby Boomers endured 4 recessions, 4 rounds of high unemployment, and erratic mortgage rates that started from a low of 7% and rose to a peak of 18%. However, those who got in the game where they could, with a long term mindset, were rewarded and are looked upon as “lucky” to have gotten in when they did.

Flash forward to 2023. While admittedly there is a large swath of buyers priced out of purchasing a home due to mortgage rates between 6.8%-7.5%, there are a number of them who have the means to enter the market but are waiting for mortgage rates to decline. Their mindset is not unlike those buyers who waited for prices to come down when rates were below 3% two years ago, and now regret it. Waiting for the perfect home, at the perfect time, at the perfect price and the perfect mortgage rate is an exhausting and futile endeavor. The reason being that when all the perfect boxes are checked off, there is a line of competing buyers that make the experience… well ...less perfect.

Jump to September. As Greater Phoenix moves into the last few months of 2023, seasonally this is the best time to be a buyer. Active listings are rising as they typically do in the Arizona Regional MLS, providing more selection. The median sales price is $40,000 below the highest peak of June 2022, and prices are stable for now. These months are typically slower than the Spring, but competing demand for homes is further suppressed by mortgage rates. Thus 41% of sales involve seller-paid closing costs that often include a rate buy-down. Closing cost assistance is one of the first things to go when rates decline and/or buyer competition increases in relation to supply. Since January, the percentage of sales with assistance has dropped from 51% to 41% and the median paid by sellers has dropped from $9,700 to $7,500.

Things aren’t perfect, but 3 out of 4 isn’t bad.

For Sellers:

Currently, the median number of days prior to a seller obtaining an accepted offer is 21 days. However, going into the last few months of the year, sellers should allow for an extra week or two as the calendar approaches year-end holidays. Historically, properties that are listed in October are on the market for a median of 2-4 days longer than those listed in September. However, properties listed in late October or early November are typically 10-14 days longer.

Real estate professionals often advise their clients that the first week of active status is the most important in terms of gauging whether a listing is priced appropriately to attract a full price offer. Analyzing the last 30 days of sales, this advice proves to be true. Properties that accepted contracts within 1 week of list showed 68% of sellers received their original list price or more at closing. At 2 weeks on the market, that measure declines to 53% but is still a majority. By week 3, however, 59% of sellers accepted offers less than their original price, and after 4 weeks on the market 81% accepted less.

As sellers approach longer marketing times in October, it’s common to see both active listings and price reductions increase. This year is following that expectation and weekly price reductions are on the rise, up 34% since the beginning of July, but still down a whopping 63% from this time last year. Weekly price reductions are expected to continue rising gradually from now until they peak in early November, so sellers planning to list within the next few weeks may want to budget for at least one in their strategy.

Make no mistake though, the market still favors sellers. So far this year, sales prices have appreciated 6-7% over the past 8 months, with 12 fewer days on market compared to last year, and tighter negotiations within just 2% of the last list price on average. Sale prices are expected to continue rising mildly for the next 3 months.

Commentary written by Tina Tamboer, Senior Housing Analyst with The Cromford Report

©2023 Cromford Associates LLC and Tamboer Consulting LLC

Living In Scottsdale